Polymarket Fee Surge Explained: Where Did 90%+ of Extreme Fees Come From?

Original Title: "Deep Dive into Polymarket's Fee Formula: How Did 90%+ Extreme Fee Rate Come About?"

Original Author: Azuma, Odaily Planet Daily

Polymarket suddenly found itself in a fee controversy.

Many community users discovered last night that when trading on Polymarket, they were charged unusually high fees, resulting in a significant reduction in received shares or earnings compared to before.

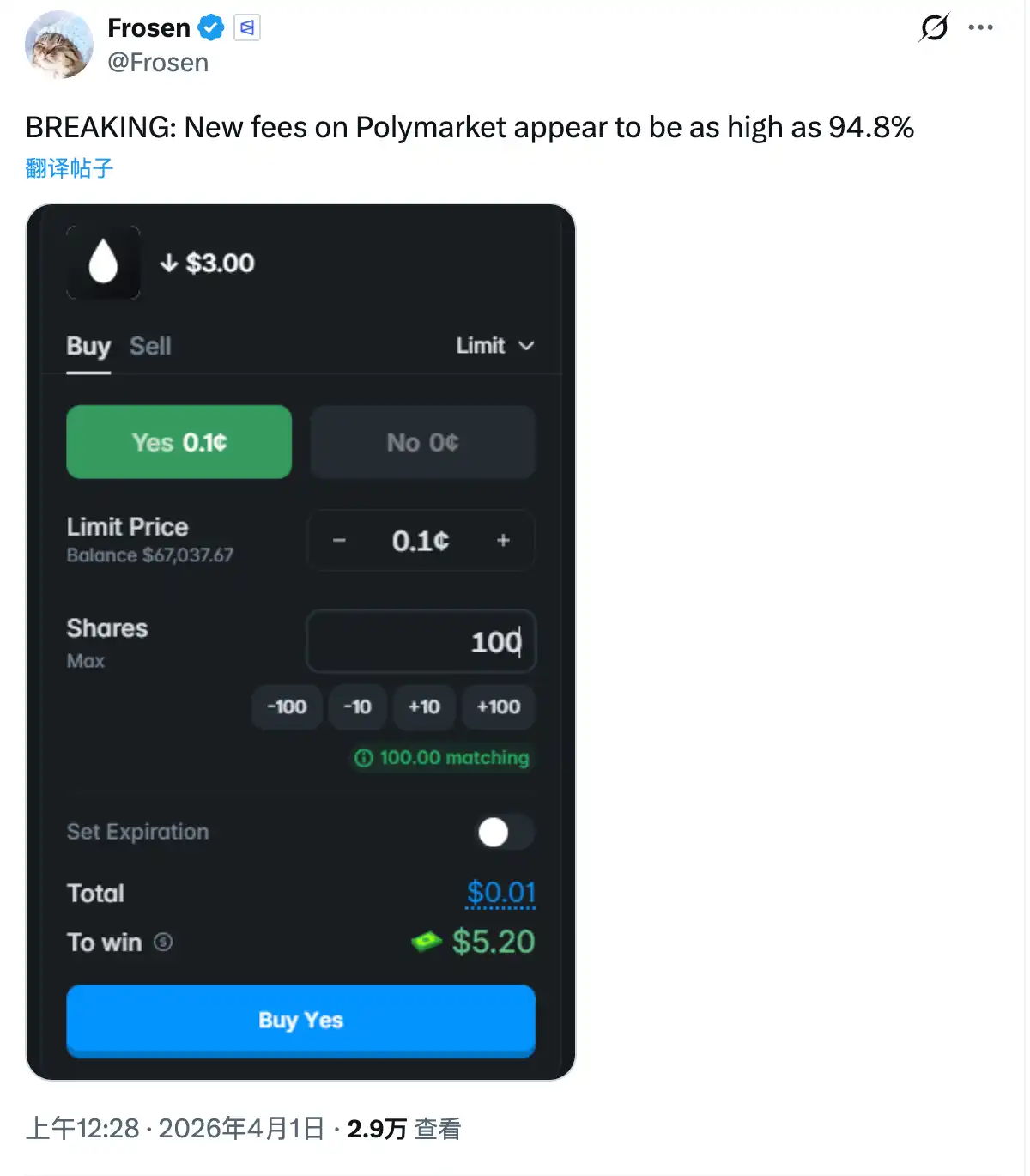

Overseas user Frosen (@frosen) even posted a screenshot, indicating that they tried to place an order for 100 shares at a price of 0.1 cents in an "economics" market, but the Polymarket frontend displayed a correct payout amount of only $5.2 (which should normally be $100) — corresponding to an outrageously high fee rate of 94.8%!

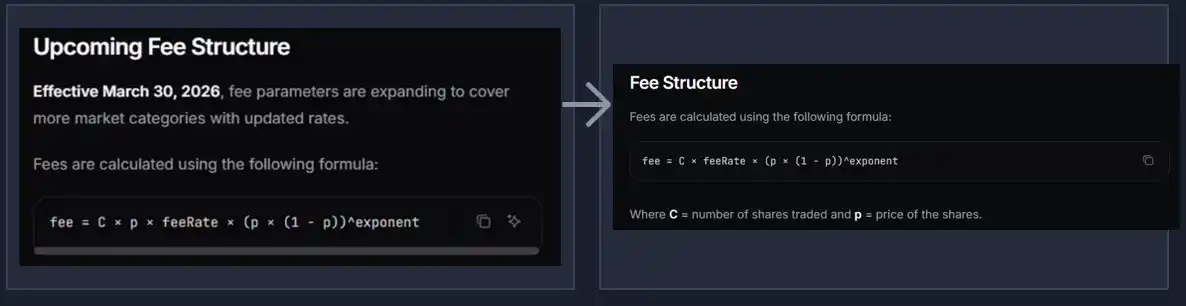

What's going on? Is Polymarket going crazy for money? Odaily, based on Polymarket's official disclosure and community investigation, found that the direct cause of this unexpected situation was that Polymarket modified the platform's fee formula last night, with three versions of changes:

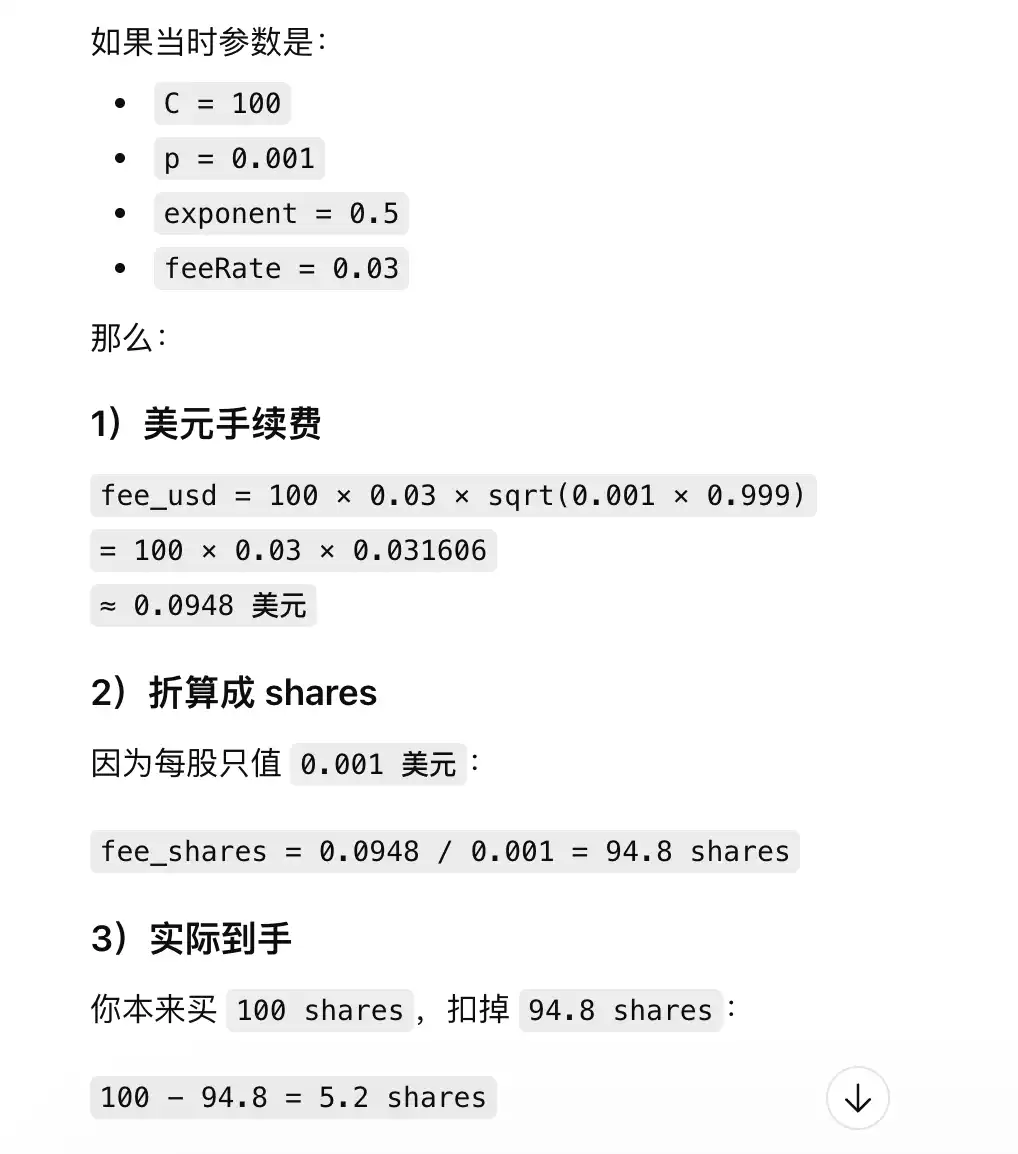

· First was the "old formula" introduced since March 30: fee = C × p × feeRate × (p × (1 - p))^exponent;

· Then came the first modification, the formula that caused the unexpected situation (referred to as the "abnormal formula"): fee = C × feeRate × (p × (1 - p))^exponent;

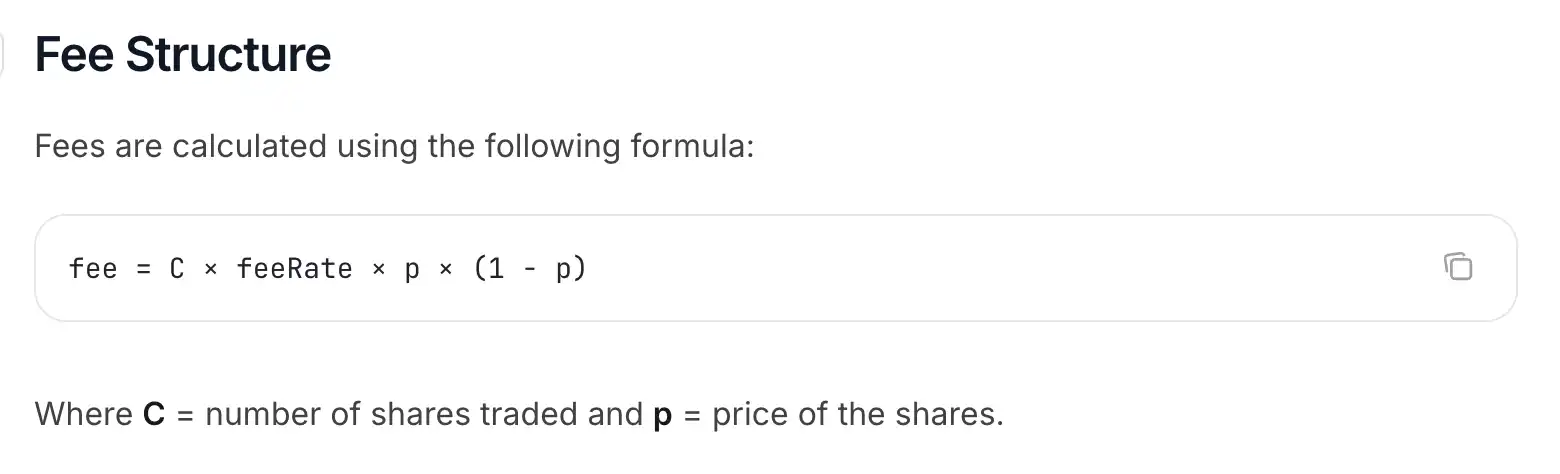

· Subsequently, after realizing the issue, Polymarket made corrections, resulting in the current version of the "new formula": fee = C × feeRate × p × (1 - p);

· It's important to note that in all three formulas, C refers to the number of shares traded, p refers to the share price, and feeRate and exponent are variables.

Decoding the Abnormal Formula, How Did the 94.8% Outrageous Fee Rate Occur?

You don't need to worry too much about the math details. By comparing the "Old Formula" and "Anomalous Formula," you can easily see that the latter only removes one "× p" (this is the multiplication symbol, not the lowercase x), meaning it ultimately multiplies the share price one less time.

Since the price of all shares on Polymarket is always less than 1 USD, this will inevitably lead to a overall increase in fees. The lower the price of shares, the more significant the fee increase due to skipping one multiplication — when the share price approaches 0, the fee rate may become absurdly high.

As for how absurd this fee can become, it also depends on the same variable ^exponent present in both the Old Formula and Anomalous Formula. Translated directly, ^exponent means "raised to the power of exponent," and this variable is mainly used to control the steepness of the fee curve.

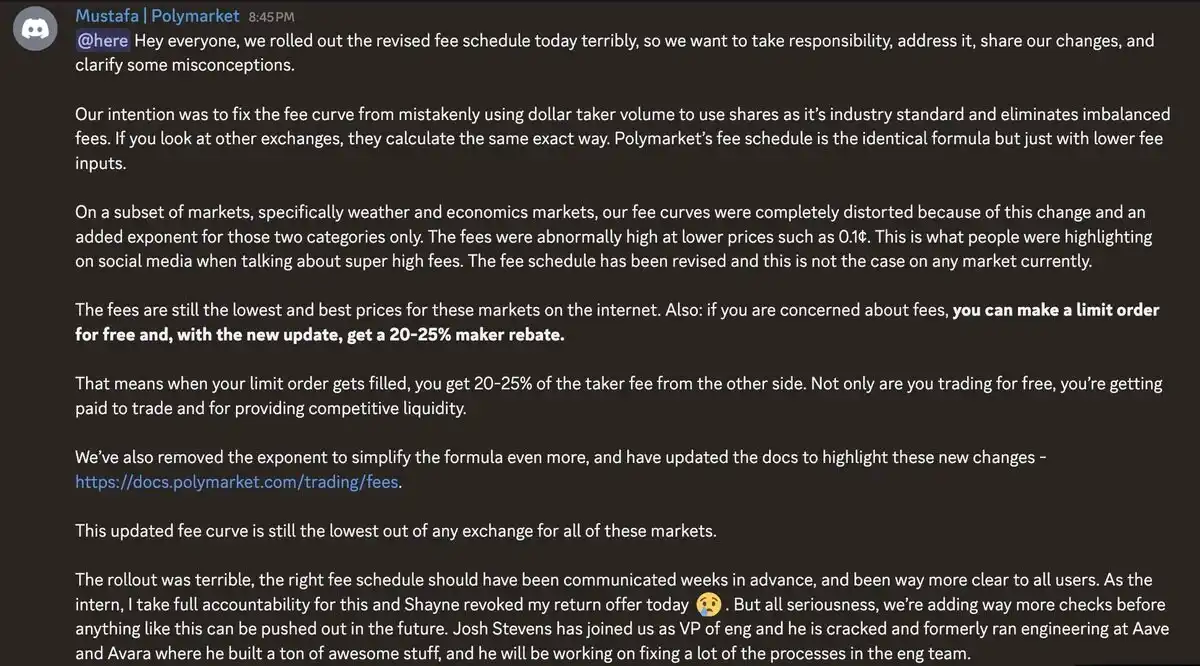

According to Polymarket staff member Mustafa, the anomaly formula introduced last night only included the exponent in two types of markets: "Weather" and "Economic." According to overseas KOL Quant Chad (@Autonomous_Chad), the exponent parameter set for these two major markets at the time was 0.5.

Now, going back to Frosen's case and plugging the corresponding numbers into the equation fee = C × feeRate × (p × (1 - p))^exponent from this anomaly formula. Knowing that C equals 100, meaning Frosen wants to place an order for 100 shares; p equals 0.001, meaning 0.001 USD (0.1 cents); exponent equals 0.5, meaning another power operation on (p × (1 - p)); the final fee rate is 94.8%.

By feeding this to an AI directly, you can reverse-engineer that the feeRate level at that time was around 0.03, while also reconstructing the formula calculation details that Polymarket applied to this order.

In simple terms, Polymarket calculated, based on the anomalous formula, that the fee for this order should be 0.0948 USD. Since Polymarket deducts the corresponding value of shares directly from the buy order, and the share price at the time was only 0.001 USD, it needed to deduct 94.8 shares. Therefore, Frosen would ultimately receive only 5.2 shares, even if the prediction is correct, the potential profit would only be 5.2 USD.

Polymarket Remedial Action

Shortly after the anomalous fee issue arose, Polymarket promptly responded by modifying the formula to its current version, fee = C × feeRate × p × (1 - p). Compared to the anomalous formula, the new formula removed the '^exponent'—effectively raising the exponent parameter from 0.5 to 1 in the anomalous formula fee = C × feeRate × (p × (1 - p))^exponent.

In the anomalous formula, the '^exponent' effect was to perform another power operation on the p × (1-p) data set. In Polymarket's actual operational scenario, the theoretical result range of p × (1 - p) is between '0.000999 - 0.25'—as p approaches 0.5 (shares price approaches $0.5), this data set gets closer to 0.25; when p approaches 0 or 1 (shares price approaches 0 or $1, with extreme quotes at $0.001 and $0.999), this data set gets closer to 0.000999.

Within the '0.000999 - 0.25' range, regardless of the value taken, raising the exponent parameter from 0.5 to 1 directly reduces the final fee result in the formula calculation, thereby decreasing the overall cost.

More importantly, this reduction has a more pronounced inhibitory effect on exceptionally high fees near very low price levels—when p × (1-p) = 0.000999, the fee under the new formula is only about 3.16% of the fee under the anomalous formula, representing a decrease of approximately 96.84%; when p × (1-p) = 0.25, the fee under the new formula is 50% of the fee under the anomalous formula.

As indicated in the Polymarket official documentation, following the implementation of the new formula, fee rates at extremes in the 'Weather' and 'Economics' market categories have now decreased to 5%.

How Can Retail Users Avoid Fees?

I know most users are lazy to look at the above formula, but are also concerned about Polymarket's current fee issue.

In response to this, Mustafa mentioned on the official Discord: "If you're worried about fees, you can place limit orders for free, and after this new update, you can also receive a 20%-25% maker rebate—this means that when your limit order is executed, you will receive 20%-25% of the taker fee, essentially enabling you to not only trade for free but also potentially earn rewards by trading and providing competitive liquidity."

So let's change our habits, try not to market buy directly anymore, switch to using limit orders more often, and you can also try using Polymarket's Split feature more frequently, indirectly build your position by selling the other side of the shares through a reverse limit order.

You may also like

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

See “Buy Walls” & “Sell Walls” Instantly: WEEX Launches the Depth Chart for Smarter Trades

What Is Quick Trade on WEEX? 2 Ways WEEX Ends Chart-Panel Jumping

Morning News | Five major virtual asset platforms in South Korea have experienced 57 incidents of hacking and system failures in six years; Grayscale submits registration application for Canton ETF

Should we escape the peak? The principle of the tail-end market in the stock market

RootData: May 2026 Cryptocurrency Exchange Transparency Research Report

Founder of Baixing.com: My Experience with Claude Code in Fourteen Points

Yang Ge Gary: Agent Economics and AI Microeconomics

When reasoning becomes a scarce resource, who captures its value?

Jensen Huang dramatically "rescues" the South Korean stock market

Stablecoins vs Deposit Tokens: On the surface, they seem like opposing sides, but in reality, they are interconnected

Bitcoin Crash to $50,000 or Bear Trap Before $100,000? Deep Dive for WEEX Traders

How Could the SpaceX IPO Affect Bitcoin, Altcoins season, and Crypto Liquidity?

The ambitions of Kalshi, MTS, and a16z

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.